Computer Guy

Active Member

- Joined

- Aug 31, 2016

- Threads

- 0

- Messages

- 35

- Reaction score

- 27

- Location

- Southwest Michigan

- Vehicle(s)

- 2017 Lightning Blue GT350

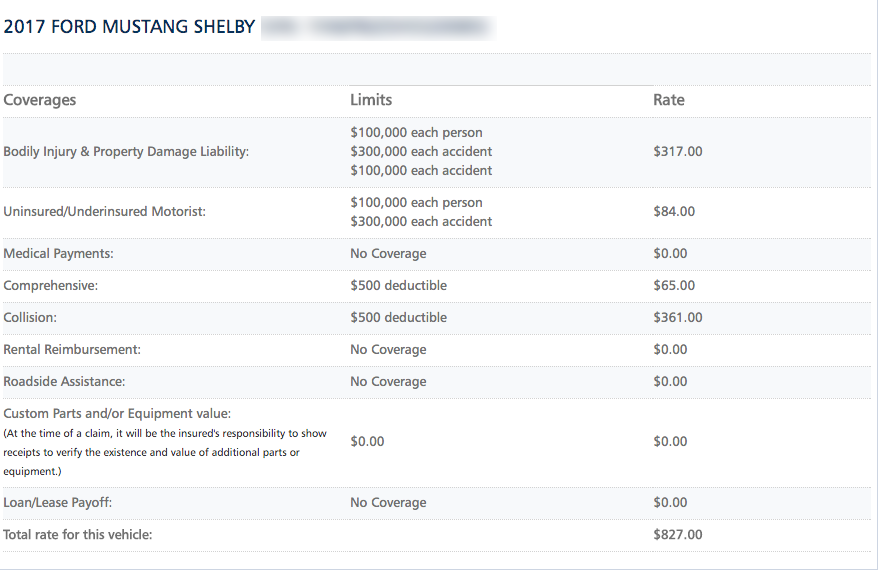

GT350s are awesome cars, but just be prepared for sticker shock when seeing the insurance bill. Six months of insurance on my 2011 Mustang GT premium has been hovering at about $520 since I bought the car new. When I bought the 2017 GT350 in July 2016, its insurance was just over $1000 for 6 months. Late last year the GT350's insurance cost symbols were updated by the insurance company, resulting in the 6 month insurance cost increasing to $1689 - so three times as expensive as the insurance on the Mustang GT. These rates are through Michigan Farm Bureau for a 40+ year old person who has never received a ticket, has never had an at fault accident, has multiple vehicles and a home insured through the same company, has had a policy with the company for 15+ years, and I am the only driver on the policy (in other words, I qualify for all of the available discounts).Matt get a 350, you wont regret it, you loved the one you review and it was a base. Just do it")

I had a lengthy discussion with the insurance agent yesterday about the price hike. The best that we could determine is that when the insurance was first put on the car, it was treated like a $61,000 Mustang GT, but now it is in its own cost category lumped into a new "most expensive Mustang" group that also covers the GT350R that with dealer markups has an insurance calculated replacement cost of $80,000 to $100,000. The insurance agent advised that his insurance company will be switching to a new insurance calculation system that is based on the car's full VIN, so there is likely to be another jump up or down in October.

The recent ~70% jump in insurance rate for the GT350 is not specific to Michigan Farm Bureau, as other people reported seeing similar jumps with other insurance companies.

Just throwing this out there as a potential warning for people who do not quality for the maximum insurance discounts due to age, tickets, accidents, etc. - owning a GT350 is not cheap.

Sponsored